The risk of inflationary pressures will continue to plague the US economic outlook

Since the start of the global inflationary shock in 2021, one of the great global uncertainties has been the trajectory of US interest rates. The Fed originally decided to wait inflation out, deeming it “transitory”, before having to change tack and hike its benchmark rate at the most aggressive pace in decades. Today, inflationary pressures have eased substantially: in June, prices grew by 3.0% YOY, down from the peak of 9.1% reached in the summer of 2022. But they remain stronger than the Fed would like: this is particularly the case in services, the consequence of a tight labor market.

We continue to expect the Fed to lower interest rates in 2024, starting around September and by no more than 75 bps. However, there remain several points of uncertainty when it comes to US inflation: today, the cost of services and housing continue to increase at a sustained pace. Meanwhile, the specter of a second Trump presidency, and the tariffs that he would seek to impose, could place upward pressure on inflation in the US. Together, these factors make Fed policy highly uncertain.

Business Implications

Businesses should plan for a slow and steady reduction in US interest rates starting from late 2024. However, they should ensure they are prepared for the possibility of interest rates remaining at their current level until well into 2025. This would constrain lending and delay recoveries in rate-sensitive sectors such as housing and manufacturing. Persistently elevated rates would also pile pressure on US consumers, particularly those on lower incomes who rely more on credit card debt, but also on mortgage-holders who would refinance at higher rates. Finally, a high interest rate environment would exacerbate pressures on highly indebted sectors, notably commercial real estate, and potentially trigger financial instability. From a global perspective, higher-for-longer US interest rates would keep pressure on foreign currencies and potentially aggravate imported inflation, as well as potentially delay central bank cuts.

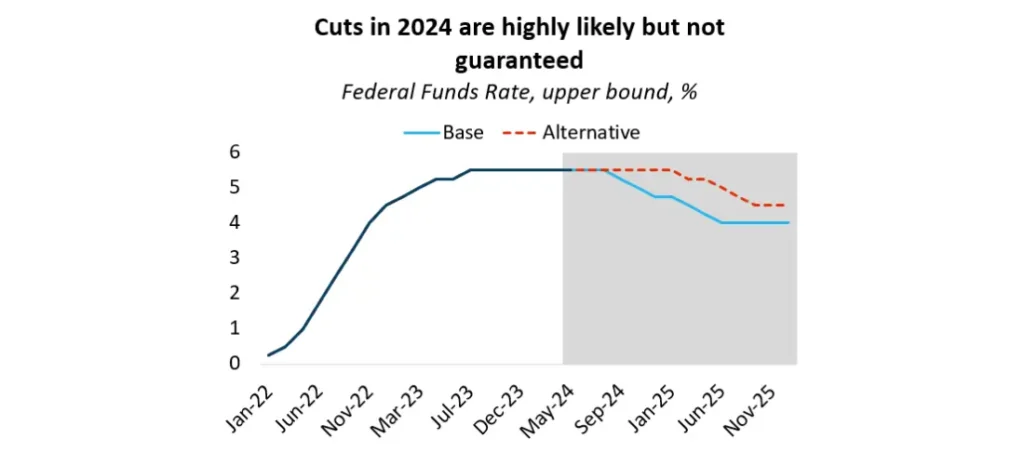

Fed Policy Scenarios:

Base case (80% probability): our base case assumes that inflation will continue to slow throughout H2 2024 and into 2025 as consumer spending slows and the labour market eases. In turn, this will allow the Fed to begin loosening its policy rate from September 2024 onwards, in a slow, cautious, and conservative cutting cycle. This scenario assumes a moderate increase in imports tariffs in 2025, with a modest upward impact on inflation. Our base case sees no more than 75bps of cuts in 2024, and between 75 and 100bps in 2025.

Downside scenario (20% probability): our downside scenario assumes further surprises from the US economy, with stronger-than-expected consumer spending and continued labor market tightness that feed into inflation. This scenario also assumes a drastic increase in import duties under a second Trump administration, notably on goods from China, which would force the Fed to take an even more cautious approach. This scenario assumes no cuts in 2024, and around 50bps of cuts in 2025.

What is stopping the Fed from starting its cutting cycle in 2024?

In the immediate term, while the makeup of inflation in the US is much more positive than it was two years ago, there remain some underlying pressures. Housing remains a significant contributor to inflation: while rent prices show signs of either stabilizing or falling in data provided by the private sector, this has yet to show up in official CPI numbers. The cost of services is the other culprit, itself the product of rapid wage growth in previous years. Some service subcategories, such as auto insurance, are still rising at a rapid pace (around 20%YOY).

What would a second Trump presidency mean for inflation and interest rates in the US?

The other main point of uncertainty when it comes to US inflation has to do with the impact of Trump’s proposed tariff policies. While we hold the view that a blanket 10% on all US imports is highly unlikely to be implemented, a second Trump administration would still seek to increase duties on several trading partners, notably China (Trump has floated the idea of a 60% tariff on Chinese goods). The magnitude of the impact depends on the extent to which Trump’s policies are applied, but will almost certainly result in higher and more entrenched inflationary pressures, forcing the Fed to keep interest rates higher.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.