China’s economic outlook varies widely under different real estate scenarios

China’s real estate sector, once a cornerstone of its economic growth, is spiraling downward. Investment and sales have seen declines of approximately 30% and 50%, respectively, since their peak in Q2 2021. This downturn has emerged as a central weakness in the nation’s economy, which previously derived nearly one-third of its activity from real estate. Given the sector’s critical role and uncertain outlook, scenario analysis is essential. It equips businesses with strategic insights necessary for navigating potential market shifts, preparing for diverse conditions, and making informed decisions amidst economic uncertainties.

Business Implications:

The real estate investment slump has drastically reduced demand for construction materials like cement, steel, glass, and chemicals, leading to substantial overcapacity. B2B companies are now experiencing heightened sales and pricing pressures in these industries. Executives should prepare for these pressures to persist and utilize our industrial overcapacity monitor to inform their pricing and demand projections. When exploring opportunities linked to real estate development, they should focus on top-tier cities and state-owned developers, which are most likely to benefit from the government’s policies.

The real estate sector’s decline, coupled with limited job creation in high-tech manufacturing, is impeding labor market recovery. Considering current sluggish trends, the job market is unlikely to normalize until late 2026. This dynamic is weighing on incomes and driving up youth unemployment. Continued declines in property prices are also eroding the wealth of affluent families with substantial property holdings, impacting their willingness to spend. Together, these factors are subduing consumer spending and prompting many households to trade down. B2C companies should consider adapting their product offering and find a balance between maintaining market share and securing profit margins during this challenging period.

A significant drop in government revenue from land sales (which once accounted for over 30% of the total) and strict controls on local government debt are restraining public spending. Although tax reforms might offer some relief in the longer term, their effectiveness in the short to medium term is likely to be limited. B2G companies should prepare for an extended period of reduced demand and heightened pricing pressures.

Companies across industries should build substantial flexibility into their China forecasts. The country’s growth outlook is highly uncertain due to the real estate market’s ongoing deterioration. Executives can use the growth estimates in our scenario analysis as a gauge for how much buffer to build into their projections.

Scenario Analysis:

Upside (15% likelihood): The central bank boosts credit provision, flooding state-owned banks with liquidity to aid developers in completing projects. Developers reinitiate construction, restructure debt, and benefit from urban village renovations. Homebuying restrictions are lifted nationwide, revitalizing property transactions. As the market stabilizes and confidence grows, house prices stabilize too.

Base case (55% likelihood): Privately owned developers in debt receive insufficient funds to finish projects, losing market share to state-owned peers. Despite local governments’ efforts to ease homebuying restrictions, create affordable housing, and promote “urban villages renovation”, plans become disorganized and face resistance. Real estate investments and house prices keep declining, denting consumer confidence.

Downside (20% likelihood): Local governments struggle to revive the property market due to limited funds. Policy coordination crumbles as house prices drop, transactions decrease in almost all cities, and private developers go bankrupt. State-owned developers take over the market, but their investments are insufficient. Huge job losses in the sector worsen consumer confidence and hinder overall growth.

Extreme downside (10% likelihood): Insufficient government funds lead to the collapse of many developers, leaving numerous unfinished projects. The state is unable to take over, triggering protests. House prices and jobs dependent on the sector disappear, causing an employment crisis and shrinking household wealth. Confidence in government declines, impacting various industries and sinking overall growth.

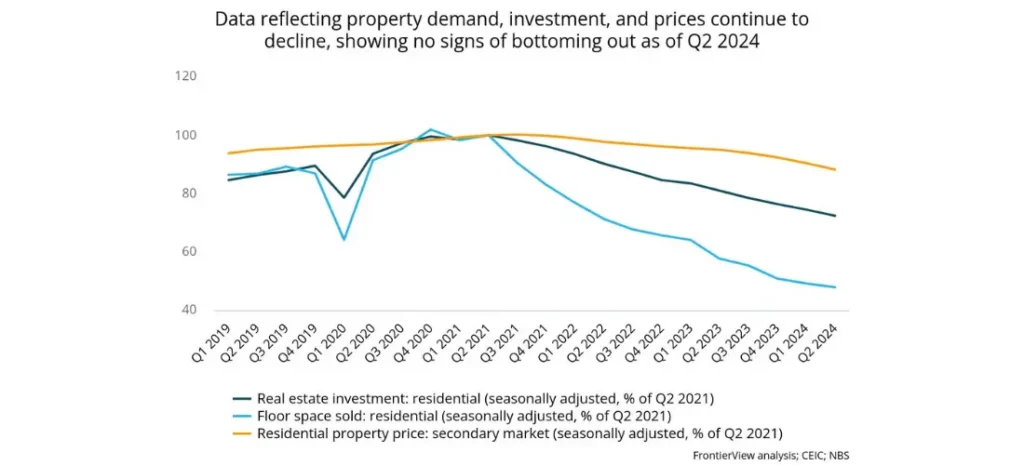

Real estate sector in Q2 2024:

China’s real estate sector continues to contract. The declines in residential real estate investment and home prices in the secondary market widened from -9.5% YOY and -5.2% YOY in Q1 to -10.5% YOY and -7.4% YOY in Q2, respectively. However, the decrease in home sales narrowed from -27.8% YOY in Q1 to -16.5% YOY in Q2. This improvement is partly attributed to the “517 New Policy,” which includes measures such as lowering the down payment ratio and mortgage rates to historic lows and enabling the central bank to provide CNY 300 billion in loans to support local-level state-owned enterprises in purchasing unsold residences for use as affordable housing. While helpful in the short term, the policy’s longer-term effectiveness remains uncertain.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.