Sticky underlying price pressures, however, may delay the pace of the cuts, but the outlook remains broadly positive

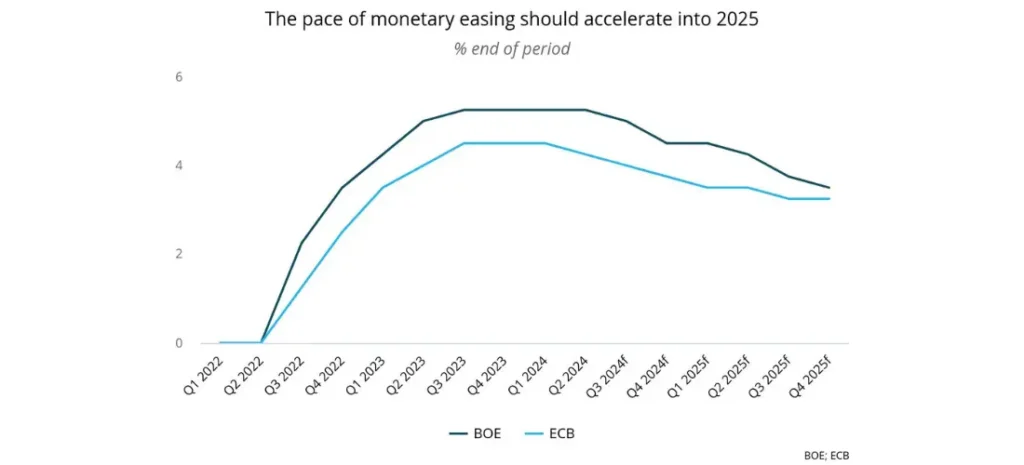

In line with our expectations, the Bank of England (BOE) introduced a 25-bps cut in August, bringing its key policy rate to 5.0%. The move follows an earlier European Central Bank (ECB) cut in July 2024, marking the beginning of monetary policy easing that will extend throughout 2025. Persisting inflationary pressures, however, will continue to prevent more aggressive rates of cuts, and a potential surprise upwards readings may delay the pace of the easing.

Business Implications:

The pace and range of the cuts will be indicative of the recovery in economic activity across Europe through 2025, especially given the tough operational and demand environments. Lending activity is set to make a more pronounced rebound and should underpin the recovery in both business and consumer demand. Easing lending rates should also alleviate pressures on distributors and channel partners, especially when it comes to outstanding debt. Executives should note that despite the relative optimistic outlook, lending rates will remain historically elevated through the rest of 2025 and will continue to pose operational challenges, especially when it comes to smaller channel partners and certain customer segments.

Looking ahead

Eurozone inflation has edged up slightly in July 2024 to 2.6% YOY from the June reading of 2.5% YOY. Weak economic activity and prolongation of deflationary pressures will likely result in another ECB cut in September and December of 25 bps, leaving the ECB’s refinancing rate at 3.75% at the end of the year. Further easing in inflation in 2025 will renew the ECB’s easing momentum and we expect the ECB to introduce a series of cuts that will bring the refinancing rate to 3.25% at the end of 2025. While we expect the BOE to introduce another cut in October as well, the decision to cut in August was not uniformly supported by decision makers, signaling persistent cautiousness. Even though inflation will edge up in Q4 2024, the BOE is likely to introduce further easing that will bring the key policy rate to 4.50% from the current 5.0% at the end of 2024. Persistent cautiousness, however, makes the outlook far less certain, and monetary authorities will slow down the pace of easing, should underlying inflationary pressures prove to be more severe.

Despite the cuts, we do not expect to see significant pressures on average on both the GBP and the EUR, given gradually improving economic conditions and the beginning of the US Feds’ cutting cycle and both currencies should broadly appreciate in 2024 when compared to 2023, with the gradual appreciation momentum likely to extend into 2025. Fiscal sustainability in the Eurozone, however, will continue to weigh on investor sentiment, and September 2024 may result in short-term volatility, as countries that have been subjected to an excessive deficit procedure are set to present their long-term plans to consolidate expenditures and reduce long-term debt.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.