Policies unveiled at China’s recent “Two Sessions” suggest an increasing focus on domestic demand over manufacturing

But lack of policy details creates uncertainty for MNCs seeking clearer revenue projections

Business Implications:

B2C Implications: Companies catering directly to Chinese consumers can expect general stabilization through 2025 in consumer confidence as a result of potential upcoming government measures. However, sales performance may vary significantly between products eligible for trade-in subsidies and those that are not. Even firms selling products or supplying to those eligible for subsidies should remain cautious, as current sales boosted by these subsidies may come at the expense of future spending. Therefore, B2C firms should be particularly cautious about revenue projections over the next 12 to 18 months.

B2G Implications: MNCs can expect their government clients to be in a slightly better fiscal position this year compared to last. Business opportunities are likely to increase, and payment cycles are expected to improve. This will also benefit MNCs’ suppliers and business partners, typically local SMEs, who have suffered from late or even non-payment from government and other state-owned clients in recent years.

Industrial sector implications: Multinational manufacturers in China should not be overly concerned about the “downgrade” of industrial production priorities in government reports. It remains the second most important task for the year, and senior leaders are likely to continue investing in the sector, particularly in high-tech and advanced manufacturing, such as electric vehicles, batteries, and green technologies. However, manufacturers should be concerned about tariffs from traditional export markets, like the US and Europe, and the speed at which they can find alternative markets. Failure to adapt could lead to increased revenue pressures this year. If that happens, they should prepare to effectively communicate any underperformance to their headquarters.

Details:

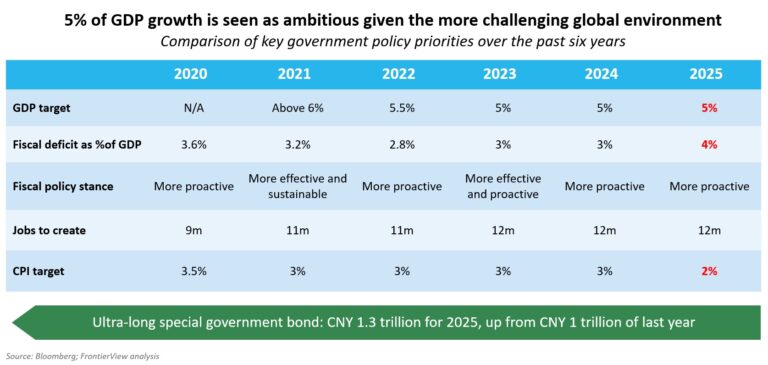

China held its most important annual legislative meeting this month, the so-called “Two Sessions”. At the event, leaders released several economic targets for 2025. Among the most important were a GDP growth target of 5% (once again), a fiscal deficit target of 4%, and an inflation target of 2%.

- A fiscal deficit of 4% is the highest in nearly 30 years, highlighting the urgency senior leaders felt in supporting the economy.

- An inflation target of 2% is the lowest in more than two decades, implicitly acknowledging the leadership’s recognition that China is now under significant pressure from weak prices.

At the meeting, China’s leaders reiterated their pledge from the Central Economic Work Conference in December last year to prioritize “boosting consumption” and “expanding domestic demand” as their top goals for 2025.

- As a result, industrial production and manufacturing development have been downgraded to the second most important task this year.

After the Two Sessions, China released combined data for the first two months of the year.

- Retail sales data showed notable improvement, with a 4.0% in the January-February period, surpassing the 3.7% increase recorded in December.

- Industrial production grew 5.9% YOY in January and February on an accumulative basis, down from 6.2% YOY in December. Fixed-asset investment increased by 4.1% YOY in the first two months of this year, significantly up from the 3.2% YOY recorded in December.

Our View:

Challenging growth target: Chinese leaders will find it even more challenging to achieve their 5% growth goal this year than last year. The tariffs from the Trump administration will almost certainly significantly impact exports, which accounted for over 30% of growth last year. Consequently, Chinese leaders will need to focus more on finding internal growth opportunities this year.

A shift of focus to boosting consumption:

- This is a strategy leaders have been urged to adopt for years but have been hesitant to implement.

- The recent shift in official rhetoric, both at the year-end Central Economic Work Conference and the “Two Sessions” this month, indicates a notable change in mentality among senior leaders.

- The shift of their focus, at least temporarily, came as tariffs from the Trump administration have made the environment for exports all the more challenging.

Lack of policy details and potential caveats:

- The “Two Sessions” lacked detailed policies on how to boost consumption, aside from a general pledge to increase workers’ wages and an announcement of a CNY 300 billion allocation to support the trade-in scheme.

- Since the introduction of the scheme last year, products eligible for trade-in subsidies, such as automobiles, home appliances, and smartphones, have experienced a sales surge. However, this surge essentially pulls forward future consumption and comes at the expense of products not eligible for such subsidies, like cosmetics, clothing, and food.

- As a result, there is a risk of future consumption slowing down and an imbalance in sales between different product types.

More debt for fiscal expenditure:

- More expenditure is necessary to reignite China’s growth, because resolving many of China’s existing structural issues requires substantial capital, such as stabilizing local governments’ debt burdens, accelerating accounts payable to local businesses, paying civil servants on time, recapitalizing state-owned banks, and halting the further decline of the property market, particularly by reclaiming idle lands already sold to developers.

- Leaders therefore have decided to increase this year’s fiscal deficit to 4%, the highest in nearly 30 years. They have pledged ultra-long special bonds worth CNY 1.3 trillion for this year and arranged the issuance of another CNY 4.4 trillion in special bonds for local governments.

- While these measures should help stabilize the domestic economic and fiscal situation for the rest of the year, the announced amounts appear insufficient to support a strong rebound in growth.

In summary, 2025 is likely to be another challenging year for China’s growth as it navigates unfavorable domestic and international conditions. Premier Li Qiang noted in his government work report at the “Two Sessions” that China’s economic performance in 2024 exhibited a pattern of “high at the beginning, low in the middle, and rising towards the end”. This pattern could repeat this year unless additional stimulus measures are implemented quickly and forcefully.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.