Interest rates, trade tensions, and energy costs could derail the sector’s fragile recovery

The improvement in global manufacturing conditions in the first quarter of 2024 is both positive and welcome news, and sets the tone for a more sustained recovery throughout the rest of the year. Still, multinationals should be cautious in their optimism: the trajectory of the global economy remains uncertain, primarily due to the path of interest rates. Should rates remain higher than expected, this manufacturing recovery could be stopped in its tracks. Executives should therefore look to monetary policy as a leading indicator of the outlook. Multinationals in the manufacturing space should also assess their exposure to industries prone to overcapacity in China, such as steel, electric vehicles, batteries, and solar panels; these sectors are expected to come under intense pricing pressure in 2024, and trade spats between China and major trading partners such as the EU are likely. Finally, manufacturers should start planning now for the possibility of a second Trump presidency, which remains our base case, and which we expect would be highly disruptive to global trade.

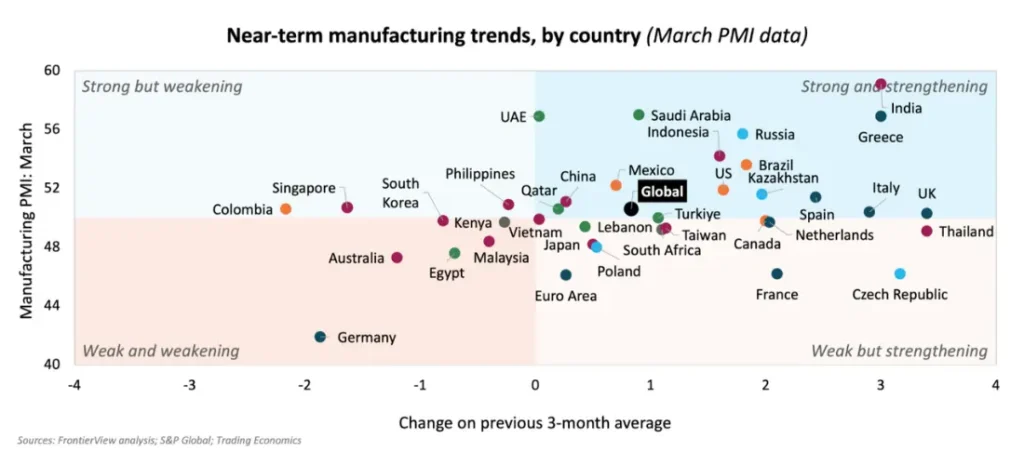

Overview

- The Global Manufacturing Purchasing Managers’ Index (PMI) came in at 50.6 in March, its highest since June 2022 and above the 50 expansion mark for the third consecutive month.

- Improvements in the Global Manufacturing Purchasing Managers’ Index (PMI) since the start of 2024 point to a tentative recovery in the manufacturing sector, following a year and a half of contraction.

- The increase comes amid renewed momentum in both output and new orders, which was seen across consumer, intermediate, and investment goods. In turn, manufacturers added jobs in line with the higher level of activity.

- From a geographic perspective, Europe (particularly Germany and France) continues to suffer, while pickups were registered in the US and China. India remains the star of the show, posting its highest PMI figure since 2008.

- At the global level, input and selling prices continued to rise, although at a weaker pace.

Our View

For the first time in several months, manufacturers have reasons to be optimistic: the global manufacturing sector expanded for the third month in a row, pointing to a tentative recovery across all sub-sectors of manufacturing.

Looking forward, we expect this recovery in conditions to gain traction, thanks to a combination of recovering purchasing power and consumer confidence, falling interest rates, and the start of the replacement cycle. Still, any optimism should be cautious, with several challenges clouding the outlook: aggressive price competition from Chinese manufacturers will place pressure on their counterparts elsewhere and is likely to lead to trade spats. Meanwhile, global oil markets remain tight and subject to geopolitical volatility—substantial increases in energy costs are not out of the question. Finally, the strength, pace, and timing of the recovery is likely to be highly divergent between, and even within, regions.

Take Europe: while the majority of markets have suffered a contraction in the past several months, signs point to a divergence in outlooks, with early signs of a recovery in output in Italy, Spain, and the UK, while German and, to a lesser extent, French manufacturers continue to grapple with anemic demand. The overall picture in Europe remains a bleak one, with the contraction in new orders on the verge of being the longest ever, surpassing the one experienced during the eurozone crisis and limiting the scope for a meaningful rebound in activity across the region in 2024. On a more positive note, the impact of Red Sea disruptions seems to be abating, with manufacturers having adapted to longer, but more predictable, lead times.

Signs of a recovery are becoming clearer in the US: the output sub-index reached a 22-month high, and new orders also grew, predominantly from domestic sources. Together, these point to a growing appetite for goods in the US, potentially the consequence of stubborn price growth in the service sector. This higher demand is strengthening the pricing power of American manufacturers, which increased their prices by the most in 16 months for consumer goods, highlighting the challenges of the return back to the US Federal Reserve’s 2% inflation target.

The Chinese manufacturing sector is also showing tentative signs of improvement, posting its strongest PMI in over a year, and the fifth consecutive expansionary figure. This is consistent with the Chinese government’s renewed focus on developing industrial production. However, manufacturers are faced with persistently sluggish domestic demand and are increasingly turning toward external markets to resolve this supply-demand imbalance. Pricing remains the predominant concern in China: low demand has all but erased pricing power, and manufacturers are having to reduce prices in order to maintain volumes. In turn, this is eroding their profitability and will continue to do so for the majority of the year; price pressures and cost management will be the name of the game in China.

Finally, emerging markets paint a more positive picture, with India once again taking the top spot as the world’s best performing manufacturing sector—its PMI was the highest in 16 years, buoyed by rip-roaring domestic demand and robust investment. Strong internal demand is also the main tailwind pushing ASEAN manufacturers forward, helping offset sluggish global demand for their products and inputs. In Mexico, manufacturers are also enjoying strong demand, although the prospect of disruptions stemming from the US election in November continues to weigh on business optimism.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.