Inflation and FX risks will prevent many central banks in the region from cutting interest rates as much as originally planned

Firms should expect credit costs in ASEAN to remain elevated this year as central banks are unlikely to adjust monetary policy significantly after raising rates over the last two years. These pressures will be the most severe in Indonesia and the Philippines, because interest rates were raised most aggressively in these markets from 2022 to 2023. Due to a tight interest rate environment, executives should consider shifting CAPEX expenses to OPEX expenses, if and where possible. Additionally, firms should prepare for challenging negotiations with distributors in the region, particularly small local distributors, who may struggle with maintaining large inventories and making additional CAPEX investments due to high interest rates.

The exception to this trend of elevated interest rates will be observed in Vietnam. Interest rates there will be near the all-time low seen from 2020 to 2022. While this will give firms some leeway to increase CAPEX spending, they should exercise caution, as demand conditions in Vietnam will be tepid this year.

Overview

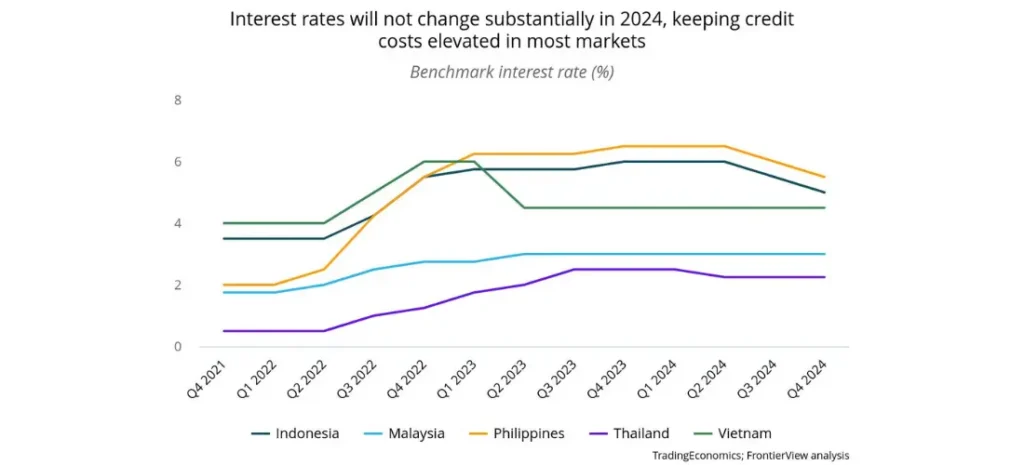

Most ASEAN central banks raised benchmark interest rates over the last two years, leading to an increase in credit costs. In recent months, these central banks have opted to keep interest rates unchanged for various reasons.

- Indonesia: Bank Indonesia (BI) left its benchmark interest rate unchanged at 6% for its fifth consecutive meeting in March 2024 due to persistent pressure on food and fuel prices as well as the depreciation of the rupiah in recent months.

- Philippines: Bangko Sentral ng Pilipinas (BSP) held its benchmark interest rate at 6.5% in February 2024 due to ongoing volatility in food and fuel prices, which has reduced its policy space for rate cuts.

- Malaysia: GDP growth weakened to 3.7% YOY in 2023 amid weak export demand, putting pressure on Bank Negara Malaysia (BNM) to cut rates. However, resilient domestic demand and a volatile ringgit have led the BNM to keep its monetary policy settings unchanged since May 2023.

- Thailand: GDP growth in Thailand has been notably sluggish over the last year due to weak exports and delays in government spending. As a result, PM Srettha has intensified calls for the central bank to cut rates, stating that the economy is in a crisis. However, the central bank has resisted such calls, arguing that current rates are conducive to long-term growth. (For details, see our analysis here.)

- Vietnam: The State Bank of Vietnam (SBV) reduced the benchmark refinancing rate to 4.5% in 2023 amid a significant growth slowdown and financing pressures in the property sector. These interest rates are close to the lowest level Vietnam has seen over the last decade. The SBV has left the refinancing rate at this level in 2024 as the economy continues to face major headwinds.

Our View

Monetary policy in ASEAN is likely to be relatively static this year. Due to varying domestic fundamentals, interest rates will either remain unchanged or be cut only marginally.

- Indonesia: Due to persistent inflation and FX risks in the coming months, the BI will likely hold rates in Q2 2024, with the downside risk of an additional rate hike of 25 basis points if the rupiah continues to depreciate. Subsequently, we expect the central bank to commence rate cuts in H2 2024 once these risks subside to a larger degree. The BI will likely cut rates by 100 basis points in H2 2024, lower than the 150 basis points earlier expected.

- Philippines: Similarly in the Philippines, due to volatile prices (especially of key commodities such as rice), as well as pressure on the peso, the BSP will delay rate cuts to Q3 and only cut by 100 basis points as well. The expected cumulative rate cuts of 100 basis points will be substantially lower than the cumulative rate hikes of 450 basis points witnessed over the past two years.

- Malaysia: Despite soft export demand, the BNM will likely leave rates unchanged this year, as strong domestic demand will continue to keep the economy afloat. The weak ringgit will be an additional reason for the BNM to keep rates on hold, as cuts would expose the currency to further depreciation.

- Thailand: The Bank of Thailand (BOT) will remain under immense pressure from the government to drastically slash rates amid weak GDP growth. However, we expect the BOT (which acts independently) to cut rates by only a marginal 25 basis points this year.

- Vietnam: The SBV will likely keep interest rates at current low levels this year, as headwinds in the form of weak exports and muted construction activity will remain through 2024.

Firms should also be mindful of potential changes in monetary policy by the US Federal Reserve, as they would influence monetary policy in select ASEAN markets. Per our base case, we expect the US Fed to cut rates by 100 basis points in 2024, starting from June. However, in the downside event that the US Fed decides to keep rates higher for longer due to stubborn inflation, central banks in Indonesia and the Philippines will likely announce smaller rate cuts in 2024 as well.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.