This is likely to lead to divergences in monetary policy

As we exit the shock of 2020–2023, a rethink of global inflationary trends is appropriate. While executives should continue to keep an eye on global sources of inflation such as oil prices, they should increasingly turn to domestic ones, such as nominal wage growth or the strength of domestic demand.

Divergent trends in inflation will, in turn, dictate the strength and speed of the recovery in purchasing power: the less time consumers spend in an environment of rapidly increasing prices, the more they can rebuild their purchasing power—the opposite holds true. Domestic drivers of inflation will also dictate the path of interest rates and, with that, the strength of activity in rate-sensitive sectors such as real estate and manufacturing.

Overview

- The main causes of the global inflationary shock that rocked the world economy in the last three years now appear to be subsiding.

- Following historically high levels of disruption following the pandemic, supply chains have returned to their historical average.

- Meanwhile, commodity prices (notably oil and gas) are largely back to their levels from before Russia’s invasion of Ukraine.

- In developed markets, labor market tightness is easing, reducing pressure on wage growth.

Our View

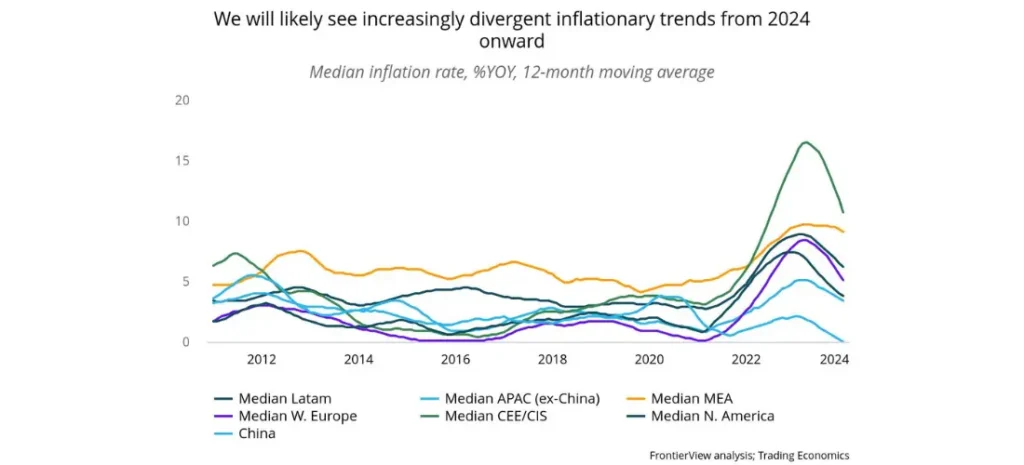

Slowly but surely, the global economy appears to be turning a page when it comes to inflation. While price growth remains an issue in most countries, both the severity and the cause of the issue are beginning to diverge.

Western Europe’s inflation is on a positive trend, thanks to the twofold impact of normalizing energy prices and sluggish demand. However, Europe remains uniquely exposed to shipping disruptions in the Red Sea, which have led to a spike in shipping costs and could prevent the path down toward central banks’ inflation target. Meanwhile, the risk of a wage-price spiral remains present in Eastern Europe.

In North America, the positive downward trend of inflation seen in the second half of 2023 appears to be stalling. The main culprit is housing: high home prices and a limited housing stock are putting upward pressure on rent prices. Pressures are particularly acute in Canada, where a wider proportion of consumers are exposed to the impact of higher mortgage rates. In the US, the highly resilient labor market continues to provide strong, albeit moderating pressure on the cost of services.

And then there is China—with consumer confidence near historical lows, property values dwindling, and economic activity struggling to pick up, businesses in the country are being forced to discount in order to keep volumes stable; as a result, the country is teetering on the edge of deflation. This effect is particularly acute in sectors where supply is aggressively outpacing demand, such as electric vehicles; major producers such as Tesla and BYD have cut the cost of their vehicles in China. With few signs of any fiscal stimulus that would jolt the economy back into action, the Chinese economy is likely to experience downward pressures on prices for the majority of 2024.

In the rest of APAC, the story is different. While we do expect price pressures to ease, the concern there remains the high price of food, notably rice, which is preventing further progress on inflation. This is particularly the case in several commodity importers such as Singapore and the Philippines, but also in exporters such as India.

The global desynchronization in inflationary patterns will, naturally, lead to a desynchronization in monetary policy; while most countries took a similar path on the way up, they are unlikely to be in such lockstep on the way down. This is already the case—Latin American central bankers are well underway with their monetary loosening cycle, but their counterparts in other regions, such as North America and Europe, are biding their time. Some have even gone the other way: the Bank of Japan recently increased its benchmark interest rate for the first time in 17 years.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.