Fiscal consolidation will remain a priority across the GCC

Multinationals can expect weaker public demand from markets including Qatar and Kuwait, as project momentum remains muted in the former and political complexities continue to hinder growth in the latter. Firms can expect a delay to the passing of the 2024/25 budget in Kuwait and prolonged timelines for infrastructure projects. Prepare for continued opportunities in Oman and Bahrain in sectors such as healthcare and manufacturing, which will remain a priority for the government. Identifying priority government spending areas across the GCC will be crucial in driving growth, alongside aligning across HQ and local partners on timelines of when the opportunity can be realized.

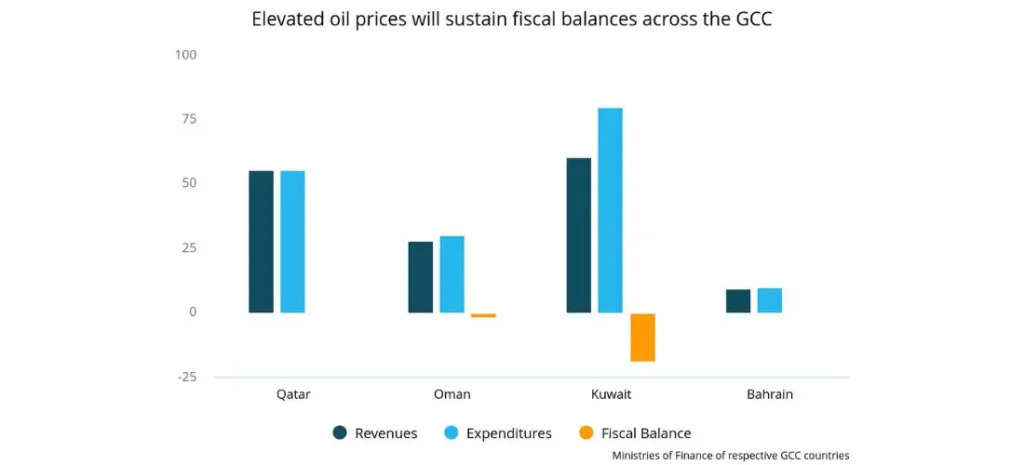

Overview

- Qatar: Total revenues are set at USD 55.4 billion, an 11.4% YOY decrease from last year’s budget amid lower energy prices. Total expenditures are set at USD 55.1 billion, a 6.3% YOY increase as the government is expected to increase debt repayments. Healthcare and education continue to be priority sectors, receiving 20% of total budget spending. The budget is based on an oil price assumption of USD 60 per barrel.

- Oman: The government’s 2024 budget estimates total revenues at USD 28 billion, up 9.5% from 2023’s budget. Total expenditures are set at USD 30.2 billion, an increase of 2.66% YOY. The government has allocated approximately OMR 900 million for development projects in line with objectives set out in the Tenth Five-Year Development Plan (2020–2025) and Oman Vision 2040. Key projects cover sectors such as transport and logistics, health, and education. The budget is based on an oil price assumption of USD 60 per barrel.

- Kuwait: The government’s 2024/2025 budget sets total revenues at USD 60.4 billion, with total expenditure set at around USD 80 billion, a drop of 6.6 YOY. CAPEX spending is expected to decrease by 15.2%.The budget is based on an oil price assumption of USD 70 per barrel.

- Bahrain: Total revenues are set at USD 9.1 billion, up 9.6% YOY compared to 2023’s budget. Total expenditures are set at USD 9.5 billion, up 0.2% YOY. The fiscal balance program remains a priority in 2024, targeting growth in the non-oil economy and aiming to increase non-oil revenues. The budget is based on an oil price assumption of USD 60 per barrel.

Our View

Overall demand for oil is soft in H1 2024, which will weigh on overall revenues, especially in Kuwait, Qatar, and Bahrain. FrontierView’s oil price assumption for 2024 is USD 82 per barrel. Subsequently, economies across the GCC will see higher-than-expected government revenues amid modest oil price assumptions of USD 60 and 70 per barrel. Despite this, we expect fiscal consolidation to remain a key aspect of governments’ public spending plans this year. Markets including Kuwait and Bahrain have a breakeven oil price above USD 85, which poses further risks to government spending outlooks, including cutting spending throughout the year alongside volatile shocks to already-existing price reduction pressures.

Expansions in LNG production will sustain government demand in Qatar, but major CAPEX spending will ease as project activity remains muted. While the country will likely record a small deficit this year due increasing debt repayments, further risks to revenue and public spending plans are highly unlikely.

Healthcare and infrastructure will remain priorities, receiving the bulk of public investments. The timely passing of a 2024/2025 budget in Kuwait remains unlikely amid the recent dissolution of the country’s National Assembly by the emir. The government will try to push forward with its recently updated four-year economic reform plan (which includes reforms to drive non-oil revenue), but progress will likely be gradual. In Oman, Vision 2040 will drive government priorities, with notably increased investments in development projects in sectors such as transport, logistics, and health. Bahrain will remain committed to its economic diversification plans—as is evidenced by the record-high FDI levels in recent months—with sectors such as manufacturing and logistics seeing increased public investments.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.